A Bubble in Narratives

Come on, come on, lovin' for the money

Come on, come on, listen to the money talk

Come on, come on, lovin' for the money

Come on, come on, listen to the money talk

In November of 2021, Silicon Valley darling shoe brand, Allbirds went public. The IPO (initial public offering) was led by Morgan Stanley, JP Morgan, and Bank of America. Allbirds peaked at a $4 billion valuation, but in its first year of a public company (2022) the stock crashed over 80%. Since the IPO, the stock has lost 99% of its value. It took less than 5 years for the company to go from a much-hyped shoe brand to near bankruptcy . In April of this year, AllBirds announced that they had sold the shoe company’s assets to the same company that runs Ed Hardy for just $39 million. In addition, they were pivoting to an AI (artificial intelligence) strategy, now called NewBirdAI. On the day of the announcement, the stock skyrocketed 600% intraday. After peaking above $24/share, the stock closed Friday at $3.83. You cant make this $hit up. This investor reaction to a failed show brand moving to AI is just further evidence that we’re in an AI bubble. But bubbles can persist for a long time. Nobody knows when the bubble will pop but comparisons to the internet craze of the late 90’s informs us of where we may be headed. I was there in ’99, and I don’t see the frenzied buying that I witnessed then, at least not yet. But I believe humans can’t help themselves and that greed and the fear of missing out (FOMO) likely propels this bubble further, maybe much further.

“The word bubble creates a mental picture of an expanding soap bubble, which is destined to pop suddenly and irrevocably. But speculative bubbles are not so easily ended; indeed, they may deflate somewhat, as the story changes, and then reflate.”

― Robert J. Shiller, Irrational Exuberance - 2000

Stories like AllBirds have me thinking a lot about Yale Professor and Nobel Prize winning economist, Robert Shiller. In March of 1999, at the absolute peak of the internet bubble, he released the NY Times bestseller, Irrational Exuberance, in which he detailed why stocks were extremely overvalued. From 2000 thru 2002 the S&P fell approximately 50%, and the tech heavy Nasdaq crashed nearly 80%. But his follow up book, Narrative Economics reminds me of how we got here. In Narrative Economics, Shiller explains that due to human nature (fear and greed), markets are actually not that efficient, as commonly acknowledged. We humans love a good story. Shiller showed that sometimes logic and math and economic fundamentals don’t matter when it comes to markets. Often, it’s the narrative (not the hard data) which gets investors to behave a certain way, even irrationally. Narratives are based on human psychology, emotion, media hype, and the virality of stories. And they can work both ways. Today many feel that AI is going to take all our jobs. This narrative is fueling the backlash to data centers and billionaires.

“We need to incorporate the contagion of narratives into economic theory. Otherwise, we remain blind to a very real, very palpable, very important mechanism for economic change, as well as a crucial element for economic forecasting. If we do not understand the epidemics of popular narratives, we do not fully understand changes in the economy and in economic behavior.” -Robert J. Shiller, Narrative Economics: How Stories Go Viral and Drive Major Economic Events - 2019

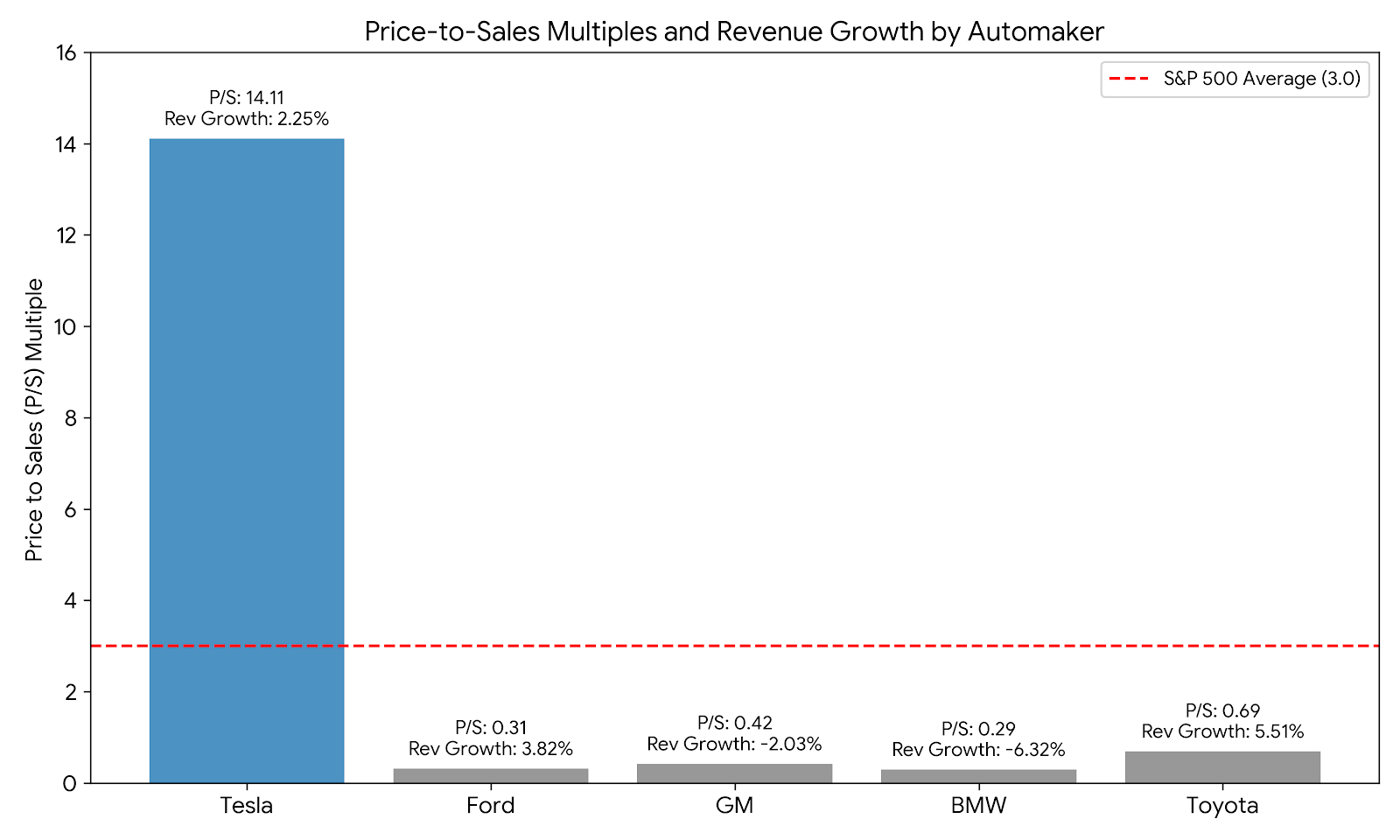

Why are Tesla investors willing to pay a sky-high multiple for the stock versus other auto manufacturers? Because Elon has effectively changed the narrative around the company. Tesla has never been viewed as just an EV maker.

Price to Sales Multiple (revenue growth):

Tesla 14.11 (2.25%)

Ford .31 (3.82%)

GM .42 (-2.03%)

BMW .29 (-6.32%)

Toyota .69 (5.51%)

(The average company in the S&P 500 trades for just 3 times sales or an 80% discount to Tesla’s 14.11. All data from Morningstar.com)

Many defenders of Tesla’s high multiple would argue that investors are paying up for future growth. Understood but today, Ford is growing revenues faster than Tesla, yet investors are paying a multiple that is 45 times greater than Ford’s. Simply put, Tesla shareholders have bought into the narrative that the company is about robots not cars. Can you imagine if the CEO of Ford announced on an earnings call that they were no longer building-150 pickup trucks because they are pivoting to humanoid robots?

This week SpaceX is expected to go public this week at a nearly $1.8 trillion valuation. It will be the biggest IPO ever, raising $75 billion. Elon’s space company is no start up. They absolutely dominate rocket launches globally and satellites in low orbit earth. The space & communications part of SpaceX (Starlink) are highly profitable with huge margins, and little to no competition in sight. However, many argue that the company is wildly overvalued due to Xai, which SpaceX bought from Elon for $250 billion in February. Xai includes AI company Grok, data centers Colossus, and X (formerly Twitter). Like most AI companies, Xai is burning lots of cash. SpaceX lost $5 billion in 2025 and has lost over $4 billion already in 2026. At a $1.8 trillion dollar valuation, SpaceX is trading at a price to sales multiple in excess of 90. Again, the average S&P company trades at sales multiple of 3. But SpaceX investors may not care about the numbers. Elon has painted a narrative that this company will among others, ensure that ‘humans will not share the same fate of the dinosaurs.’ According to SpaceX, data centers will be built and maintained in space in order to harness more of the sun’s energy and humans will become interplanetary. Nobody does narratives like Elon. But if the SpaceX IPO is like many hot IPO’s of the past, there is a good chance that you’ll get the opportunity to buy the shares significantly below it’s IPO price in the future. This is not a forecast, its speculation. I’m guessing like everyone else you’re watching on the net. But Elon’s story telling has a track record. Tesla shares are up 25,000% since the company’s IPO in 2010. SpaceX bears beware!

AI has already overtaken too much of the financial markets. It has driven most of the gains in the stock market over the past few years. The tech sector represents nearly 40% of the S&P 500. If you include Meta, Google, and Amazon (which are no longer classified as tech) the sector represents nearly half of the S&P 500. When the AI bubble finally pops, I suspect there will not be too many places to hide. Diversification is vital. We’ve been leaning into our ‘Global Aging’ and ‘Global Growth’ themes as sort of an anti-AI allocation. Within these megatrends, can be found companies without nosebleed valuations. Companies that are delivering real results today and not pitching another narrative.

I look forward to discussing further.

Thank you!

-randy

The opinions expressed in this communication are for general informational purposes only and are not intended to provide specific advice or recommendations for any individual or on any specific security. It is only intended to provide education about the financial industry. To determine which investments may be appropriate for you, consult your financial advisor prior to investing. Any past performance discussed during this communication is no guarantee of future results. Any indices referenced for comparison are unmanaged and cannot be invested into directly. As always please remember investing involves risk and possible loss of principal capital; please seek advice from a licensed professional.

Advisory services are only offered to clients or prospective clients where Hamilton Wealth, LLC and its representatives are properly licensed or exempt from licensure. No advice may be rendered by Hamilton Wealth, LLC unless a client service agreement is in place.