Future-proof Your Child: Education, AI, and 529's

"The secret of getting ahead is getting started." — Mark Twain

Today is May 29th — National 529 Day.

We mark it every year, as a reminder of the importance to prepare our kids for the future.

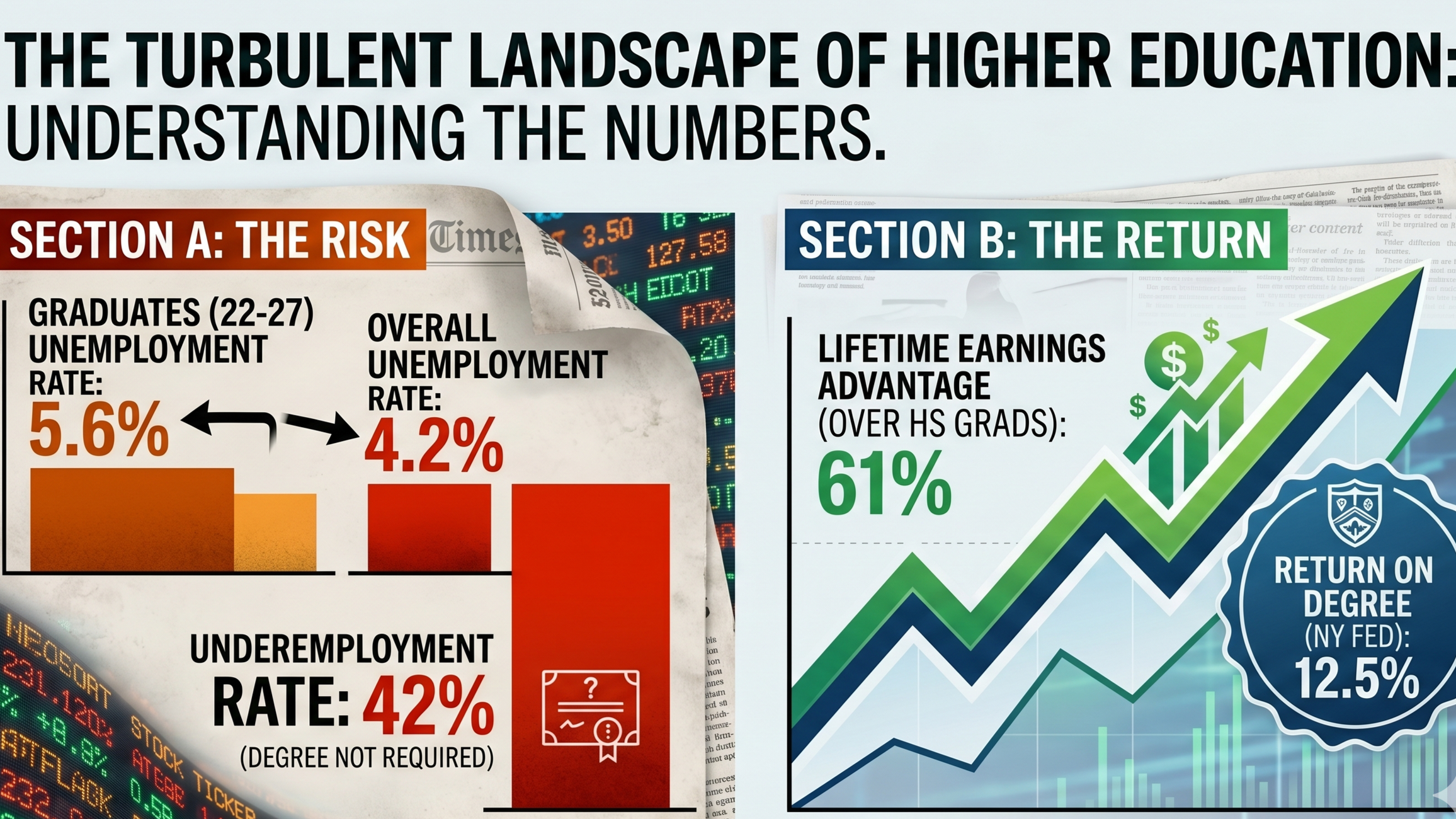

We've been warning for years about rising debt from college and the risk to future jobs due to robotics and AI. The risk to jobs seems to be coming faster and faster, which we can see in the numbers (Debt & Robots). The current unemployment rate stands at 5.6% (despite a good economy) for graduates aged 22-27. This is higher than the overall unemployment rate of 4.2%. The good news is that this rate is lower than the 7.8% experienced by those without a college degree. Also concerning is the fact that 42% of college graduates are 'underemployed'. This means they have a job, but that job does not require to have a college degree. These young adults are being forced to accept jobs to make ends meet. None of this is a reason to panic. It is a reason to plan — and to think carefully about what kind of education actually prepares a young person for what's ahead.

So how do we beat this?

Nothing is 100% foolproof, but the best thing we can do is plan, both financially and academically. Higher education is going through one of its most turbulent stretches in memory. Federal funding cuts have hit universities from Harvard to Stanford. The political conversation around campus culture isn't going away. And 63% of Americans in a recent NBC News poll said they don't believe a four-year degree is worth the cost.

We understand the skepticism. But college graduates still earn 61% more than high school graduates over their careers, and the Federal Reserve Bank of New York puts the return on a college degree at around 12.5% — outperforming most traditional long-term investments. The conversation isn't "college vs. nothing." It's "the right path, planned for wisely."

https://www.extern.com/post/best-paying-ai-proof-majors-us-2025

So, what should kids actually study?

The most reassuring answer to that question came this week from one of the last people you might expect. And while we touched on this awhile back with “What Should the Kids Actually Study,” we’ll double-click on Jensen Huang for emphasis:

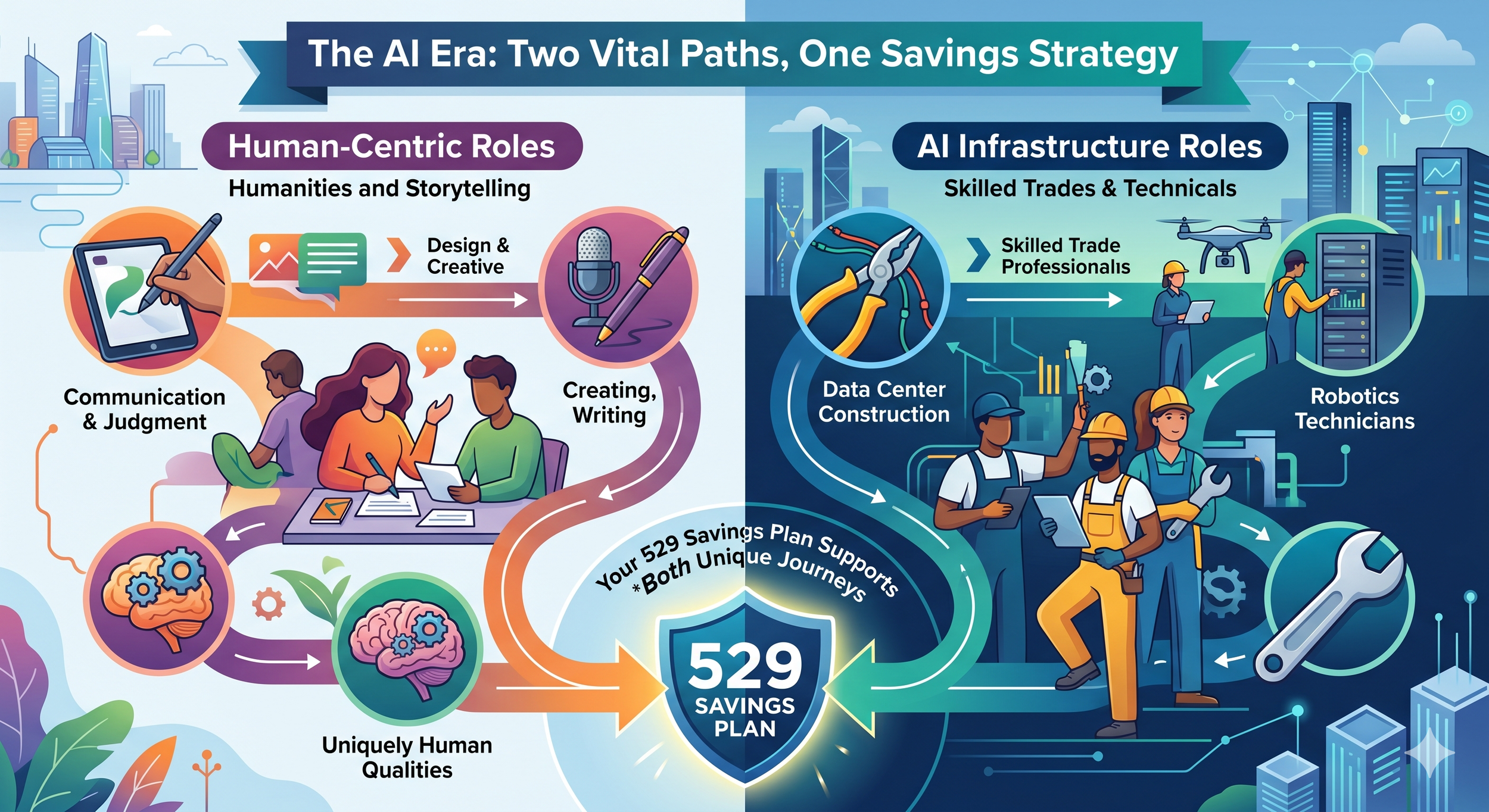

Jensen Huang is the CEO of Nvidia — the $5.2 trillion company building the chips that power the AI revolution. He says that parents shouldn't worry about what their kids study. "I think that it won't matter," he said. "All the things that used to matter are still things that are going to matter in the future." He specifically named journalism, storytelling, and design as fields that will remain valuable. Jenson also noted — at his Carnegie Mellon commencement speech earlier this month — that the AI buildout itself will require plumbers, electricians, and ironworkers to build the factories and data centers the new era demands. "No generation has entered the world with more powerful tools — or greater opportunities — than you," he told graduates. "Run. Don't walk."

https://finance.yahoo.com/news/worried-ai-become-plumber-says-122621986.html?

Daniela Amodei, co-founder of Anthropic, who studied literature at UC Santa Cruz, put it plainly: "I actually think studying the humanities is going to be more important than ever." Her argument: AI already has tremendous technical knowledge. What it still needs help with are the uniquely human qualities — communication, judgment, critical thinking.

AI boom is fueling demand for skilled trades—and demand for technicians, HVAC workers, and electricians is soaring, with six-figure salaries to match.

The lack of supply of skilled workers to build America’s rapidly growing AI infrastructure is actually pushing blue-collar wages to new highs. Construction workers on data center projects currently earn an average of about $81,800 annually, or $39.33 an hour—roughly 32% more than those on non-data center builds—according to data from Skillit, an AI-powered hiring platform for construction workers.

Demand for robotics technicians has jumped 107%, HVAC engineers increased 67%, and construction roles grew by 30% since late 2022, according to an analysis of more than 50 million job postings by Randstad. Roles like welders and electricians are also on the rise, up 25% and 18% over the past three years, respectively.

The goal isn't to engineer your child toward a specific major. It's to make sure they're educated, adaptable, and fluent in the tools of their era. And whether that path leads through a four-year university, a trade program, or a credentialing track, there's a vehicle to save for it.

Whether they become an IT expert, health care professional, or plumber, there is a cost to becoming experts in these occupations.

We recommend 529 Savings Plans as the best vehicles for saving for education (not just college). There's a reason the 529 has been around for 30 years (since 1996), because they work. There are currently 17 million 529 savings accounts with $525 billion dollars in assets. We consider them the best way to save due to their tax advantages. The contributions grow tax deferred, and withdrawals for qualified education expenses come out tax free!

Here's what the numbers look like.....

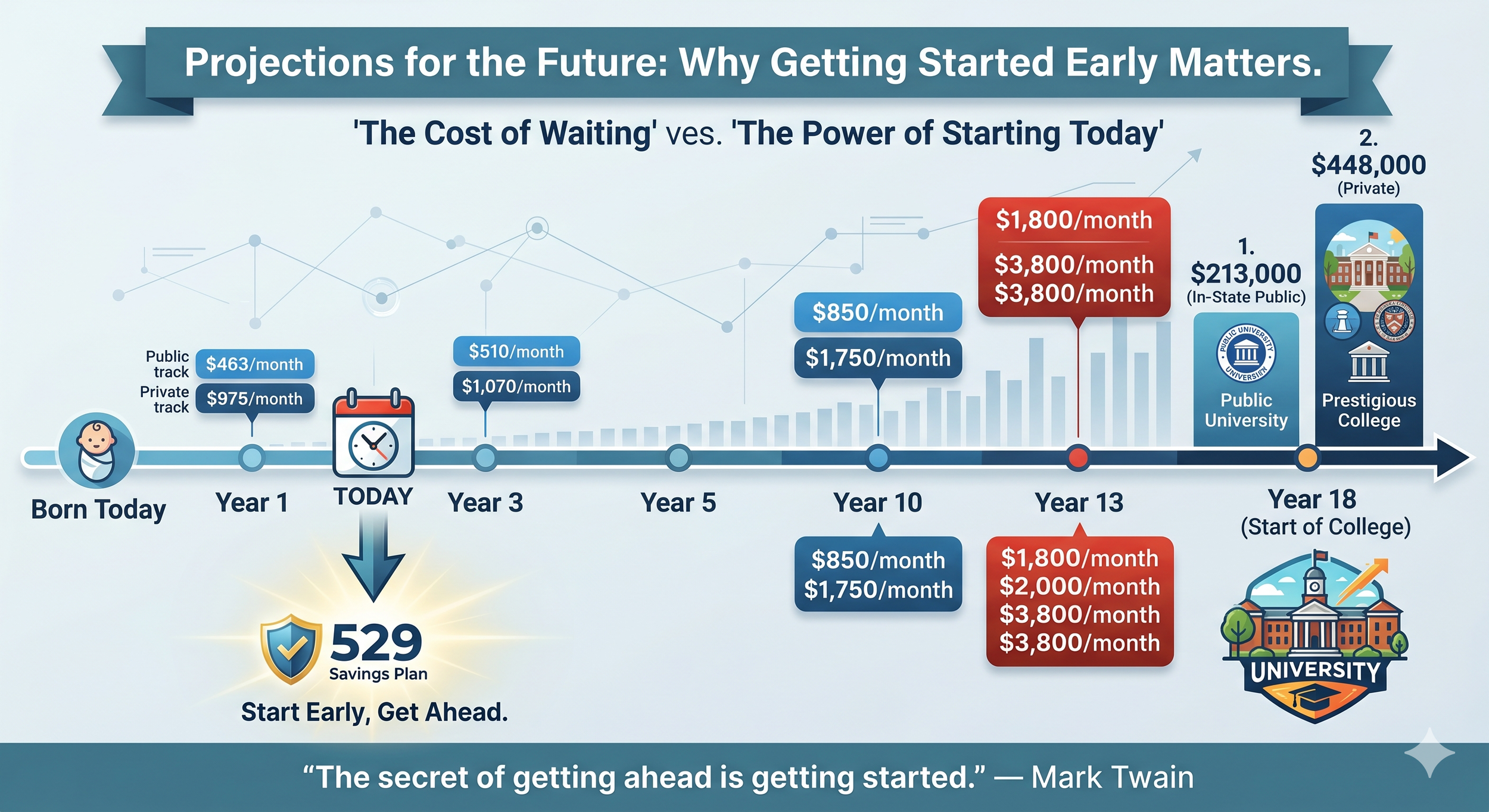

A child born today will need roughly $213,000 in 18 years for a 4-year in-state public university — or $448,000 for a private university. Reaching those targets requires saving approximately $463/month for public and $975/month for private. Sobering, yes. But manageable when you start early.

Since their creation, the rules have continued to expand, based on the changing career paths and technology. This gives more reassurance that there are ways and options to use these assets.

The assets may also be used for:

K-12 private education expenses. The annual withdrawal limit increased from $10,000 to $20,000 per child, and the definition of "qualified" now extends well beyond tuition — tutoring, test prep fees, educational therapies (including support for learning differences like ADHD), curriculum materials, and dual-enrollment fees all qualify.

Trade school and credentials are qualified expenses. 529 funds can be used for welding programs, plumbing certifications, CDL training, CPA exam prep, bar exam fees, and other credentialing programs. As the definition of education evolves, so does the 529.

Roth IRA constributions. Under SECURE 2.0, if a 529 has been open at least 15 years, unused funds can be rolled into a Roth IRA for the same beneficiary — up to $35,000 lifetime. If rolled into a Roth IRA at age 22, growing at 7% in a balanced portfolio, becomes approximately $408,000 by age 60. All tax-free. The old fear — "what if my kid doesn't go to college?" — has a real answer now. Unused savings can kickstart your child's retirement, tax-free, for decades.

529 plans aren't just for parents — grandparents, relatives, and family friends can all contribute. There are no income limits to open an account. And as of 2026, the range of qualified expenses is broader than it has ever been.

We use Vanguard to establish these accounts — low-cost, straightforward, and effective. And Hamilton Wealth does not bill on these child-specific assets.

We're happy to run projections for any school or help you get started. Whether your child is 3 or 13, the best time is always before the window gets smaller.

And that time — as Twain would remind us — is today.

—Jerry

The opinions expressed in this communication are for general informational purposes only and are not intended to provide specific advice or recommendations for any individual or on any specific security. It is only intended to provide education about the financial industry. To determine which investments may be appropriate for you, consult your financial advisor prior to investing. Any past performance discussed during this communication is no guarantee of future results. Any indices referenced for comparison are unmanaged and cannot be invested into directly. As always please remember investing involves risk and possible loss of principal capital; please seek advice from a licensed professional.

Advisory services are only offered to clients or prospective clients where Hamilton Wealth, LLC and its representatives are properly licensed or exempt from licensure. No advice may be rendered by Hamilton Wealth, LLC unless a client service agreement is in place.