Jobless Growth

Oh, our Minneapolis, I hear your voice

Singing through the bloody mist

We'll take our stand for this land

And the stranger in our midst

Here in our home, they killed and roamed

In the winter of '26

We'll remember the names of those who died

On the streets of Minneapolis

Streets of Minneapolis - Bruce Springsteen

Despite today’s headline that the U.S. economy grew 130,000 jobs in January, far above expectations, I still believe the biggest threat to the 3-year bull market and our economy is the weakness in employment. American corporations have significantly slowed the pace of hiring. Perhaps it’s the uncertainty around government policy (such as tariffs). Many corporations, including Goldman Sachs, Amazon, and Morgan Stanley are using AI or artificial intelligence to reduce headcount. Forbes described the challenging environment for recent college graduates a crisis. Way back in September last year respected economist Mark Zandi was warning us of a ‘jobs recession’:

“You can connect the dots between economic policy and the weak economy, the trade policy—higher tariffs—and the restrictive immigration policy are weighing heavily on the economy and lifting inflation…This really feels like a jobs recession…” America’s Job Growth has Flatlined - Fortune (9/5/2025)

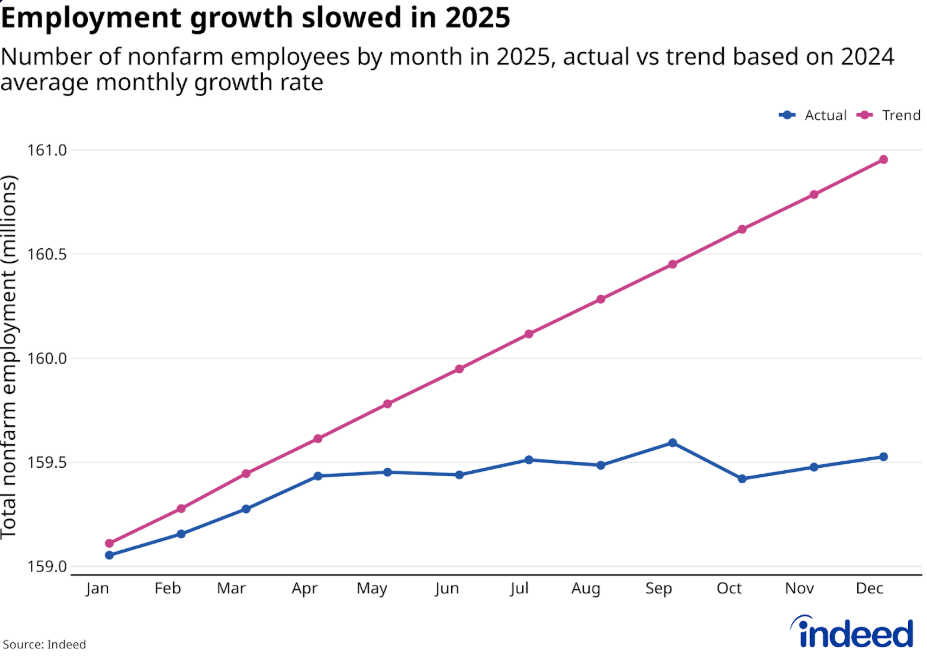

Most troubling of today’s employment report is that job growth for 2025 was revised down to just 181,000 jobs from an initial reports of 584,000. This represents a 90% decrease from 2024 when we saw job gains in excess of 2 million during Biden’s last year in office. Job gains remain concentrated in healthcare and social assistance, but we lost jobs in manufacturing and professional services. In other words, if it wasn’t for aging Boomers, we had zero job growth last year! The stock market is a leading indicator, and apparently investors are not fooled by a rising stock market. Last year, America’s biggest retailers (Walmart being the exception) saw their stocks sit out the double-digit rally in the S&P 500 last year:

Amazon, +5%

Walmart, +25%

Costco, -5%

Target, -26%

Home Depot, -9%

Kroger, +4.4

(source: Morningstar.com)

The S&P 500 was up nearly 18% last year. I suspect that the weakening jobs market may force consumers to go down market to Walmart.

Source: Hiring Lab at Indeed.

“…according to updated 2025 numbers, the economy gained a paltry 181,000 jobs for the entirety of last year (2025), revised down from the earlier reported growth of 584,000 jobs — the slowest pace of job growth outside a recession since 2003. “ Emma Ockerman – Yahoo Finance (2/11/2026)

Unfortunately, the weakness in jobs last year is spilling over into 2026. According to Challenger, Gray and Christmas, U.S. based employers announced 108,435 job cuts in January, an increase of 118% over January of 2025. It was the worst January since 2009 during the Great Financial Crisis. The number of job openings fell to 6.5 million in December, the lowest in over 5 years. Keep in mind that this data from Challenger is based on companies letting go of workers. Today’s jobs data from the government is based on household surveys.

Some good news, economic growth remains above trend according to recent reports. Goldman Sachs is more positive than most on our economy. They expect the U.S. economy to continue to grow above consensus due to tax cuts, waning effects of tariffs, deregulation, and interest rate cuts by the Federal Reserve. Speaking of interest rates, trump recently nominated Kevin Warsh to succeed Chairman Jerome Powell. Despite my reservations due to Warsh being highly political, he was a Federal Reserve governor during the Great Financial Crisis of 2007-2009. Of all the crashes, recessions, and crisis I’ve witnessed over my 33-year career, it’s usually the independent Federal Reserve, as opposed to the president or congress, that gets us on the road to recovery.

“We see the labor market as the most uncertain piece of the 2026 outlook. We see a period of jobless growth similar to the ‘jobless recovery’ of the early 2000s as a plausible alternative scenario.” -- David Mericle, chief U.S. Economist Goldman Sachs

That ‘jobless recovery’ that Goldman speaks of coincided with an S&P 500 that went nowhere for 10 years, a lost decade. It was the ‘bust’ after the internet ‘boom’ which saw the S&P 500 average minus 1% per year for 10 years. Will we see a similar bust following the AI boom? Perhaps, but timing this is impossible. What helped investors during this challenging decade was diversifying overseas. We have significantly raised our international exposure over the past year. Overseas markets handily beat the S&P 500 last year (up 32% vs 18%) and are surging ahead of U.S. stocks again this year.

President trump’s big brutal bill raised ICE’s budget from $10 billion to $85 billion. That same bill cuts spending on healthcare for millions of Americans. Despite campaigning on ‘America First’, trump appears more concerned with Iran, Gaza, Panama, Venezuela, the 2020 election, and Bad Bunny. Instead of spending billions of tax dollars on ICE, our government should focus on the weakening jobs market, which is likely to worsen in the age of artificial intelligence. The racist autocrat in the White House may get his get his interest rate cuts after all, not because he bullied Federal Reserve Chairman, Jerome Powell, who has done an outstanding job, but because of his very own lousy policies.

Now is not the time to be without a financial plan. Our government (like most in the West) is in a ballooning debt crisis. We will be forced to grow and ‘inflate’ our way out of this massive fiscal hole. In this environment you want to hold assets: stocks, commodities, real estate, precious metals. If building wealth long term is the objective, then dollars in the bank are not the security blanket you think they are. I believe they will continue to erode by inflation and a weakening US Dollar.

I have no predictions for 2026, but I am concerned by the weakness in the jobs market.

Lest discuss further.

Thank you!

-randy

The opinions expressed in this communication are for general informational purposes only and are not intended to provide specific advice or recommendations for any individual or on any specific security. It is only intended to provide education about the financial industry. To determine which investments may be appropriate for you, consult your financial advisor prior to investing. Any past performance discussed during this communication is no guarantee of future results. Any indices referenced for comparison are unmanaged and cannot be invested into directly. As always please remember investing involves risk and possible loss of principal capital; please seek advice from a licensed professional.

Advisory services are only offered to clients or prospective clients where Hamilton Wealth, LLC and its representatives are properly licensed or exempt from licensure. No advice may be rendered by Hamilton Wealth, LLC unless a client service agreement is in place.